Business

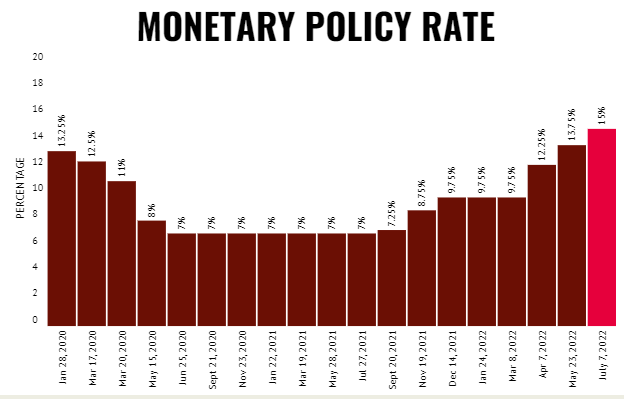

Monetary policy: SBP jacks up interest rate to 15% — highest since November 2008

- SBP has cumulatively increased the rate by 800 basis points since Sept 2021 to control inflation.

- MPC to meet next on August 22; will carefully monitor developments affecting prospects for inflation.

- Central bank expects rate hike to help prevent de-anchoring of inflation expectations, provide support to rupee.

KARACHI: In line with the market expectation, the State Bank of Pakistan (SBP) on Thursday aggressively raised the benchmark interest rate by a massive 125 basis points to 15% — the highest since November 2008.

The rate hike came as the coalition government is trying hard to revive the much-awaited International Monetary Fund (IMF) for the resumption of a $6-billion loan programme that had been stalled since early April.

The central bank has cumulatively increased the rate by 800 basis points since September 2021 to control inflation and narrow the current account deficit.

During today’s meeting, under the chair of Acting Governor Dr Murtaza Syed, it was decided that the interest rates on export finance scheme (EFS) and long-term financing facility (LTFF) loans are now being linked to the policy rate to strengthen monetary policy transmission while continuing to incentivise exports by presently offering a discount of 500 basis points relative to the policy rate.

According to a statement issued by the central bank, this combined action continues the monetary tightening underway since last September, “which is aimed at ensuring a soft landing of the economy amid an exceptionally challenging and uncertain global environment.”

“It should help cool economic activity, prevent a de-anchoring of inflation expectations and provide support to the rupee in the wake of multi-year high inflation and record imports,” the statement read.

Three major developments since May

The central bank noted that since the last meeting, the Monetary Policy Committee noted “three encouraging developments”.

- The unsustainable energy subsidy package was reversed and an FY23 budget centered on strong fiscal consolidation was passed which has paved the way for completion of the on-going review of IMF programme

- A $2.3 billion commercial loan from China helped provide support to foreign exchange reserves, which had been falling since January due to current account pressures, external debt repayments and paucity of fresh foreign inflows

- Economic activity remained robust, with the momentum of the last two years of near 6% growth carrying into the start of FY23.

However, the MPC noted that several adverse developments overshadowed this aforementioned positive news.

It stated that globally, inflation is at multi-decade highs in most countries and central banks are responding aggressively, leading to depreciation pressure on most emerging market currencies. While domestically, as energy subsidies were reversed, both headline and core inflation increased significantly in June, rising to a 14-year high.

‘Pakistan facing large negative income shock’

“Against this challenging backdrop, the MPC noted the importance of strong, timely and credible policy actions to moderate domestic demand, prevent a compounding of inflationary pressures and reduce risks to external stability,” the statement read.

The MPC members stated that like most of the world, “Pakistan is facing a large negative income shock from high inflation and necessary but difficult increases in utility prices and taxes.”

The central bank believes that without decisive macroeconomic adjustments, there is a significant risk of substantially worse outcomes that would compromise price stability, financial stability and growth.

Hinting at further monetary policy tightening in the next meeting scheduled to be held on August 22, the MPC noted that the runaway inflation and foreign exchange reserves depletion would require sudden and aggressive tightening actions later that would be significant “more disruptive for economic activity and employment.”

“Adjustment is difficult but necessary in Pakistan, as it is all over the world. However, in the interest of social stability, the burden of this adjustment must be shared equitably across the population, by ensuring that the relatively well-off absorb most of the increase in utility prices and taxes while well-targeted and adequate assistance is provided to the more vulnerable,” it stated.

“The MPC will continue to carefully monitor developments affecting medium-term prospects for inflation, financial stability, and growth and will take appropriate action to safeguard them,” the central bank said.

Enhancing Pakistan-Bahrain Collaboration: Tarar Highlights Fortifying Media Connections Between Pakistan and Bahrain

Mandi Bahauddin District Jail: MNA Launches Improvement Initiatives at Jail

Under the auspices of Ombudsman Punjab, an awareness seminar was held at the Government Mc High School in Nakana Sahib.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News2 days ago

Latest News2 days agoUnder the auspices of Ombudsman Punjab, an awareness seminar was held at the Government Mc High School in Nakana Sahib.

-

Latest News2 days ago

Latest News2 days agoPRBC Delegation Calls PM Shehbaz: PM Directs Committee Formation to Address Retailers’ Concerns

-

Latest News2 days ago

Latest News2 days agoRoad Extension Project: Bugti Launches Quetta Road Extension Project

-

Latest News2 days ago

Latest News2 days agoMandi Bahauddin District Jail: MNA Launches Improvement Initiatives at Jail

-

Latest News2 days ago

Latest News2 days agoEnhancing Pakistan-Bahrain Collaboration: Tarar Highlights Fortifying Media Connections Between Pakistan and Bahrain

-

Latest News2 days ago

Latest News2 days agoBarrister Saif: Imran will never be involved in any deal like Nawaz

-

Latest News2 days ago

Latest News2 days agoSindh Canal System: $120 million project launched by the provincial government with WB support

-

Latest News2 days ago

Latest News2 days agoSenate Session: Rana Tanveer: Government Is Not Closing Utility Stores