Business

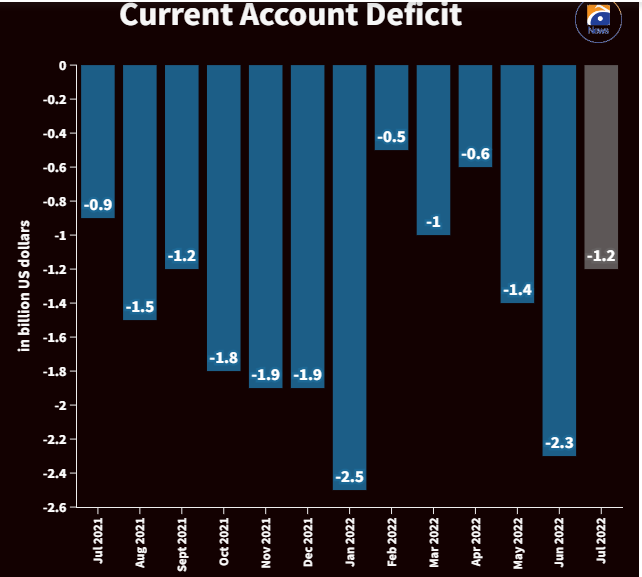

Pakistan’s current account deficit shrinks by 45% to $1.2bn

- Decline in current account deficit largely reflects a sharp decline in energy imports.

- “Narrower deficit is the result of wide-ranging measures taken in recent months,” SBP notes.

- Primary reason behind yearly deficit is a decline in remittances.

KARACHI: The three-month import ban imposed by the coalition government bore fruits as Pakistan’s current account deficit — the gap between the country’s higher foreign expenditure and low income — shrank by a massive 45% month-on-month.

The current account deficit clocked in at $1.21 billion in July 2022 in comparison to a deficit of $2.2 billion (revised figure) in June, data released by the State Bank of Pakistan (SBP) showed.

“The current account deficit shrank to $1.2 billion in Jul from $2.2 billion in June, largely reflecting a sharp decline in energy imports and a continued moderation in other imports,” the central bank said in a brief note released on its Twitter handle.

“The narrower deficit is the result of wide-ranging measures taken in recent months to moderate growth and contain imports, including tight monetary policy, fiscal consolidation and some temporary administrative measures.”

On a year-on-year basis, the primary reason behind the deficit was an 8% (yearly) decline in remittances along with a 0.4% (year-on-year) increase in total imports to $6.2 billion.

However, total exports increased by 4% year-on-year during July. Data showed that imports of goods stood at $5.39 billion in July, compared to $7.03 billion in June. At the same time, imports of services stood at $790 million in July compared to $1.32 billion in June.

Previously, widening the current account balance being an important indicator of Pakistan’s economy led to an outflow of US dollars, which had put additional pressure on the currency that has continued to struggle against the greenback.

SBP, PBS trade figures reveal discrepancies

However, the SBP and Pakistan Bureau of Statistics (PBS) trade figures revealed discrepancies. The data available showed that SBP imports exceed PBS imports in the first month of the fiscal year (July) — “a seldom event seen historically”.

According to the data released by the central bank, the total imports of the petroleum group clocked in at $2.4 billion while the figures of the bureau highlight the amount of $1.4 billion — reflecting a difference of $984 million.

Similarly, for the textile group, SBP data showed that the imports were around $379 million while PBS said that the imports clocked in at $309 million — which calculates to a difference of $70 million.

Supreme Court annuls trials of civilians in military courts

Sea conditions ‘very high’ as Cyclone Tej moves towards northwestward

IMF condition: ECC set to green light gas tariff hike today

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

WATCH: Pakistani traveller deported from Dubai for damaging plane mid-air

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team