Business

Gold extends downward spiral in Pakistan

- Gold price declines by Rs700 per tola,

- Per tola rate settles at Rs197,300.

- Silver price remain unchanged.

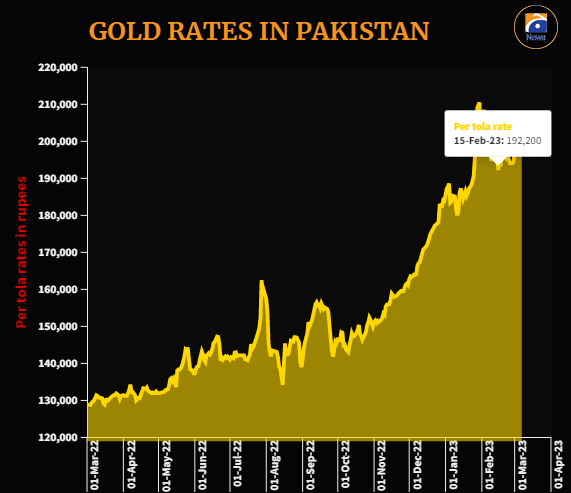

Gold extended its downward spiral on Tuesday for the fourth consecutive session as the Pakistan rupee continues to strengthen against the US dollar in both — interbank and open markets — fading the shine of the yellow metal.

The price of gold (24 carats) fell by Rs700 per tola and Rs600 per 10 grams to settle at Rs197,300 and Rs169,153, respectively, according to All-Pakistan Sarafa Gems and Jewellers Association (APSGJA).

The price of yellow metal fell Rs9,200 per tola in four trading sessions which was more than the amount it cumulatively gained Rs5,900, or 3.03% per tola during the week ended March 4.

The price of gold is declining due to the strengthening of the rupee which settled at 277.87 against the US dollar in the interbank market today after a meagre increase of 0.02% compared to Monday’s close of 277.92.

The precious commodity scaled to an all-time high of 210,500 per tola on January 30, 2023; however, the gold price started receding after the rupee recovered on hopes of revival of the $6.5 billion International Monetary Fund (IMF) bailout programme.

It should be noted that Pakistan meets almost all its gold demand through imports, and traders follow its international price in setting rates in the country. Jewellers import the metal against the US dollar and UAE dirham before converting its price into rupees.

Meanwhile, silver prices in the domestic market remained unchanged at Rs2,140 per tola and Rs1,834.70 per 10 grams, respectively.

In the international market, the gold prices eased, as investors awaited Federal Reserve Chair Jerome Powell’s testimony later in the day for clues on the future path of US interest rate hikes. The price of per ounce gold settled at $1,842 after a decline of $7.

Prices have eased from a more than two-week peak of $1,858.19 hit on Monday but remained hemmed in a narrow range.

The dollar index gained 0.1%, making bullion less affordable for overseas buyers.

Powell is due to deliver his semi-annual testimony before Congress on Tuesday and Wednesday. The US jobs report for February is due on Friday.

Gold’s quest to extend gains is set to be heavily influenced this week by potential policy clues from Powell’s testimonies and the incoming US payrolls report, said Han Tan, chief market analyst at Exinity.

If Friday’s jobs data shows significant resilience in the US labour market, it would pave the way for even higher US rates and could unwind the month-to-date gains garnered so far by gold, Tan added.

Despite being known as an inflation hedge, higher interest rates dent bullion’s appeal as they increase the opportunity cost of holding a zero-yield asset.

Supreme Court annuls trials of civilians in military courts

Sea conditions ‘very high’ as Cyclone Tej moves towards northwestward

IMF condition: ECC set to green light gas tariff hike today

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

WATCH: Pakistani traveller deported from Dubai for damaging plane mid-air

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team